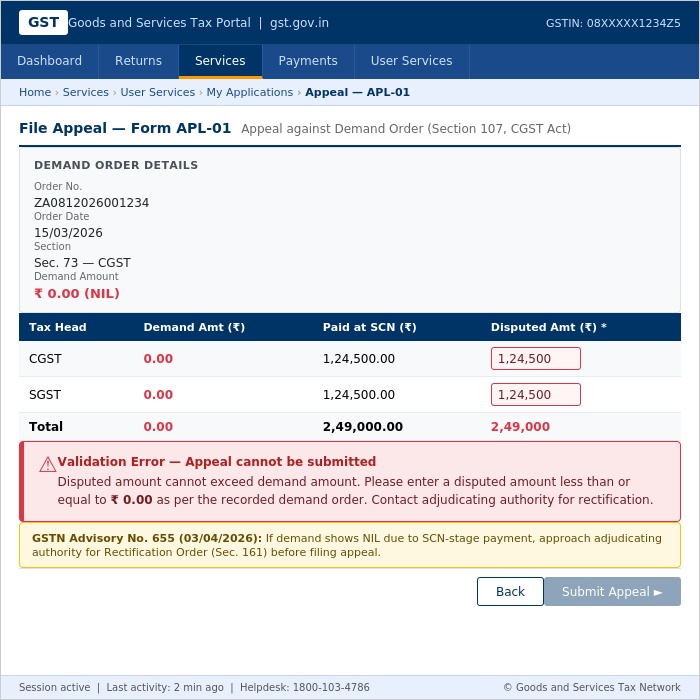

You paid the tax at the Show Cause Notice stage. You never admitted liability. Then the adjudication order arrived and showed a demand of zero. When you tried to file an appeal, the GST portal rejected it with one line: "Disputed amount cannot exceed demand amount."

This is not a one-off glitch. It is a documented, portal-wide problem that GSTN officially acknowledged through Advisory No. 655, dated 3 April 2026. If your GST appeal is blocked because of a NIL demand order, you are not alone. More importantly, you have not lost your right to appeal.

I have worked through multiple GST notice and appeal cases for clients across sectors. This specific NIL demand block has become one of the most common reasons appeals stall in 2026. This guide explains exactly why it happens, what the law says, and the precise steps to fix it before your limitation window closes.

What Is the NIL Demand Order Issue Under GSTN Advisory 655?

The NIL demand order issue is a GST portal error where an adjudication order shows zero demand, even though a genuine tax dispute exists. It occurs when a taxpayer pays tax, interest, or penalty at the SCN stage without admitting liability, and the adjudicating authority later records the payment as full discharge. The portal then blocks Form APL-01 because the Demand and Collection Register (DCR) entry is zero-valued.

GSTN's Advisory No. 655, published on 3 April 2026, formally recognized this as a system-level limitation, not a taxpayer error. When an order-in-original is passed, the GST portal generates a Demand ID in the Demand and Collection Register (DCR). If the order records NIL demand, the DCR entry is zero-value. The disputed amount field in Form APL-01 then cannot exceed zero, which blocks the appeal entirely.

This is a critical distinction. Paying tax at the SCN stage without admitting liability is a common and legally valid strategy taxpayers use to stop interest accrual. Officers sometimes close the order as 'fully paid' without recording the actual disputed amount. That single administrative entry is what creates the appeal block months later.

Why Does This Happen So Often?

Adjudicating officers work through high case volumes. When a taxpayer pays the full amount at the SCN stage, the system and the officer both register the matter as settled. The underlying dispute over whether the tax was ever legally due in the first place gets no entry in the order. The DCR records zero. The portal follows the DCR, not the taxpayer's legal position.

Does Paying Tax at the SCN Stage Mean You Have Accepted the Demand?

No. Under GST law, a payment made at the Show Cause Notice stage, without an explicit written admission of liability, does not constitute acceptance of the demand. The taxpayer retains the full statutory right to contest the liability and file an appeal under Section 107 of the CGST Act, 2017. GSTN Advisory 655 confirms this position clearly at the portal level.

This is the single most important legal clarification in Advisory 655. GSTN states plainly that such payments do not waive the right to appeal. Section 107 of the CGST Act gives every aggrieved person the right to challenge an adjudicating authority's order, and that right survives a NIL-demand technical block on the portal.

The Central Board of Indirect Taxes and Customs (CBIC) has consistently held in prior circulars that voluntary payments made without admission of liability do not foreclose future litigation. Advisory 655 applies this established principle specifically to the portal-level problem that taxpayers now face.

How to Protect Your Right at the Payment Stage

If you are making a payment at the SCN stage right now, add a written note to the challan or attach a covering letter stating that the payment is made under protest, without admission of liability, and without prejudice to your right to appeal. That single sentence, documented at the time of payment, becomes critical evidence when you request a rectification order later.

Taxpayers who had this written record in place resolved their rectification requests noticeably faster than those who had no such documentation. The officer cannot then argue the payment implied acceptance.

How Do You Fix a Blocked GST Appeal When the Demand Shows NIL?

To fix a GST appeal blocked by a NIL demand order, the taxpayer must request a rectification order from the adjudicating authority under Section 161 of the CGST Act. The rectification order corrects the demand amount in the Demand and Collection Register. Once the DCR reflects the actual disputed liability, Form APL-01 becomes available for filing within the statutory time limit under Section 107.

Here is the step-by-step process.

-

Step 1: Confirm your case fits this specific pattern. Your adjudication order must show NIL or zero demand despite a genuine dispute. The payment must have been made at the SCN stage without any written admission of liability.

-

Step 2: Draft a written rectification request addressed to the adjudicating authority. Cite GSTN Advisory No. 655 dated 3 April 2026 by name and number. Attach a copy of the payment challan and any written record showing the payment was made under protest.

-

Step 3: File the rectification request through the GST portal. Navigate to: Services > User Services > My Applications > Rectification of Order. Filing through the portal creates an official timestamped record and puts formal pressure on the officer to act.

-

Step 4: Once the rectification order is issued and the DCR reflects the correct demand amount, file Form APL-01 within the prescribed time limit under Section 107. The portal block will no longer apply.

What If the Officer Refuses to Issue a Rectification Order?

If the adjudicating authority declines, escalate the matter in writing to the jurisdictional Commissioner, citing GSTN Advisory 655 and the legal position under Section 107. If that does not resolve the matter, a writ petition before the High Court under Article 226 of the Constitution of India remains a viable remedy. At this stage, professional GST litigation support is strongly advisable, since the facts of each refusal differ significantly.

Why Does the Limitation Period Matter So Much in NIL Demand Cases?

The appeal limitation period under Section 107 of the CGST Act runs from the date the original order is communicated, not from the date a rectification order is issued. The Appellate Authority can condone delay by a maximum of one additional month beyond the three-month primary period. If the rectification process runs long, the limitation window can close before the taxpayer can file Form APL-01.

This is the detail that turns a manageable problem into an irreversible one. A taxpayer waits for the rectification process, and by the time the corrected order arrives, the three-month window under Section 107 has nearly closed. The one-month condonation window then becomes the only safety net.

The Madras High Court has held in multiple cases that the limitation period for filing an appeal can be calculated from the date a rectification application is dismissed, where the taxpayer pursued rectification in good faith. The Punjab and Haryana High Court has adopted a similar liberal interpretation. However, the Allahabad High Court has taken a stricter view, ruling the CGST Act is a self-contained code and limitation periods are absolute beyond the statutory condonable period. This judicial divergence makes acting early the safest strategy.

Document every step of the rectification process with dates: when the request was submitted, every officer communication, and portal screenshots showing the original block. If a delay was caused by the rectification process itself, apply to the Appellate Authority for condonation of delay, citing the technical block and GSTN Advisory 655 as the documented cause.

How Does the NIL Demand Issue Connect to the GSTAT Backlog Deadline?

The GST Appellate Tribunal (GSTAT) became operational in 2026 after a long delay. A transitional deadline of 30 June 2026 applied to second appeals against orders communicated before 1 April 2026. Taxpayers dealing with NIL demand blocks at the first-appeal stage who also had adverse first appellate orders faced compounding pressure from both the portal blockage and the GSTAT deadline.

Tax professionals have reported that technical synchronization issues between the GST portal and the GSTAT e-filing system added further delays for many taxpayers, including those already dealing with NIL demand blocks at the first-appeal stage. Approximately 8,400 appeals had been submitted nationally by May 2026 against professional estimates of 4 lakh eligible cases, according to industry reporting.

If your case involves both a NIL demand block at the first-appeal stage and an adverse first appellate order already in hand, treat the situation as urgent. The two timelines interact and neither pauses for the other.

Trust and Authority: What This Means in Practice

In handling GST notice and appeal matters, the NIL demand issue is rarely about bad faith from tax authorities. It is a data-entry gap at the adjudication stage that the portal's rigid logic then locks in place. GSTN's own advisory confirms this is a system limitation. That confirmation gives taxpayers a documented, official basis to push for correction rather than relying on informal arguments with field officers.

Key insight from direct case experience: taxpayers who had written proof of 'payment under protest' at the time of the original SCN payment resolved their rectification requests faster and with fewer escalations than those with no such record. The single most impactful thing a taxpayer can do before the order is issued is document the intent of the payment.

The CBIC has consistently held in prior circulars that revenue authorities cannot treat a payment as an admission of guilt unless the taxpayer explicitly states so. Advisory 655 simply applies that same principle to a portal-level technical problem that GSTN itself created and acknowledged.

Conclusion

A GST appeal blocked by a NIL demand order is a fixable, well-documented problem. Three things matter most:

-

Your right to appeal under Section 107 survives a NIL demand order. GSTN Advisory 655 confirms that payment at the SCN stage without admitted liability does not waive this right.

-

The fix requires a written rectification request to the adjudicating authority, filed through the GST portal, citing Advisory 655 and attaching your payment challan.

-

The limitation clock does not pause for rectification delays. Track your timeline from the date of the original order and apply for condonation proactively if the process runs long.

If you are facing a blocked GST appeal right now, acting early protects both your legal position and your filing deadline. The portal block is a technical problem with a legal solution. Use it.

Facing a Blocked GST Appeal or a NIL Demand Order?

Get a professional case review before your appeal window closes.

Call: +91-8588808388 | WhatsApp: +91-7217254194

LegalDev.in | Expert GST Notice and Appeal Assistance

Frequently Asked Questions (FAQs)

Q1. Can I still file a GST appeal if my demand order shows NIL?

Yes. GSTN Advisory 655 dated 3 April 2026 confirms that your right to appeal under Section 107 of the CGST Act, 2017 is fully preserved even when the portal shows a NIL demand due to prior payment at the SCN stage. The portal block is a technical limitation, not a legal bar. You must first obtain a rectification order from the adjudicating authority, after which Form APL-01 becomes available for filing.

Q2. Why does the GST portal show the error 'Disputed amount cannot exceed demand amount'?

This error appears because the adjudicating authority recorded a NIL or zero demand in the Demand and Collection Register (DCR) on the GST portal. When the demand is zero, the portal's logic does not allow the disputed amount field in Form APL-01 to be greater than zero, which blocks the appeal entirely. The fix is a rectification order under Section 161 that corrects the DCR entry to reflect the actual disputed liability.

Q3. Does the appeal limitation period pause while I wait for the rectification order?

No. The limitation period under Section 107 of the CGST Act runs from the date of the original order, not from the date a rectification order is issued. The Appellate Authority can condone delay by a maximum of one additional month beyond the three-month primary period. Madras High Court and Punjab and Haryana High Court have held that time spent pursuing a bona fide rectification application may be excluded from limitation, but the Allahabad High Court takes a stricter view. Document every step of your rectification process with dates to support a condonation application if needed.

Q4. What if the adjudicating authority refuses to issue a rectification order in a NIL demand case?

If the adjudicating authority declines to issue a rectification order, escalate the matter in writing to the jurisdictional Commissioner, citing GSTN Advisory No. 655. If that does not work, a writ petition before the jurisdictional High Court under Article 226 of the Constitution of India is an available legal remedy. Courts have intervened in cases where the portal blockage caused injustice and the taxpayer had documented proof of payment under protest. Consult a GST litigation professional at this stage.

Q5. How do I file a rectification request on the GST portal for a NIL demand order?

Log in to the GST portal at gst.gov.in. Go to Services, then User Services, then My Applications, then Rectification of Order. Select the relevant demand order and submit the rectification request with supporting documents, including your payment challan and a covering letter citing GSTN Advisory No. 655 dated 3 April 2026. Filing through the portal creates an official timestamped record and initiates formal action from the adjudicating officer.

Q6. What is GSTN Advisory 655 and why does it matter for GST taxpayers?

GSTN Advisory No. 655, issued on 3 April 2026, is an official communication from the Goods and Services Tax Network acknowledging a portal-level technical problem that prevents taxpayers from filing appeals when adjudication orders show NIL demand due to prior voluntary payment at the SCN stage. The advisory is significant because it confirms the problem is a system limitation, not a taxpayer error, and establishes that the right to appeal under Section 107 is preserved. Taxpayers can cite this advisory when approaching adjudicating authorities for rectification orders.

Author Bio

Rohit is a GST compliance specialist at LegalDev with hands-on experience resolving GST notices, adjudication disputes, and appeal filings for businesses across India. He has guided clients through Show Cause Notice responses, rectification requests under Section 161, and first appellate proceedings under the CGST Act. Rohit regularly tracks GSTN advisories and portal changes to keep clients ahead of procedural pitfalls.